Fund Selection — March 2026

Panel

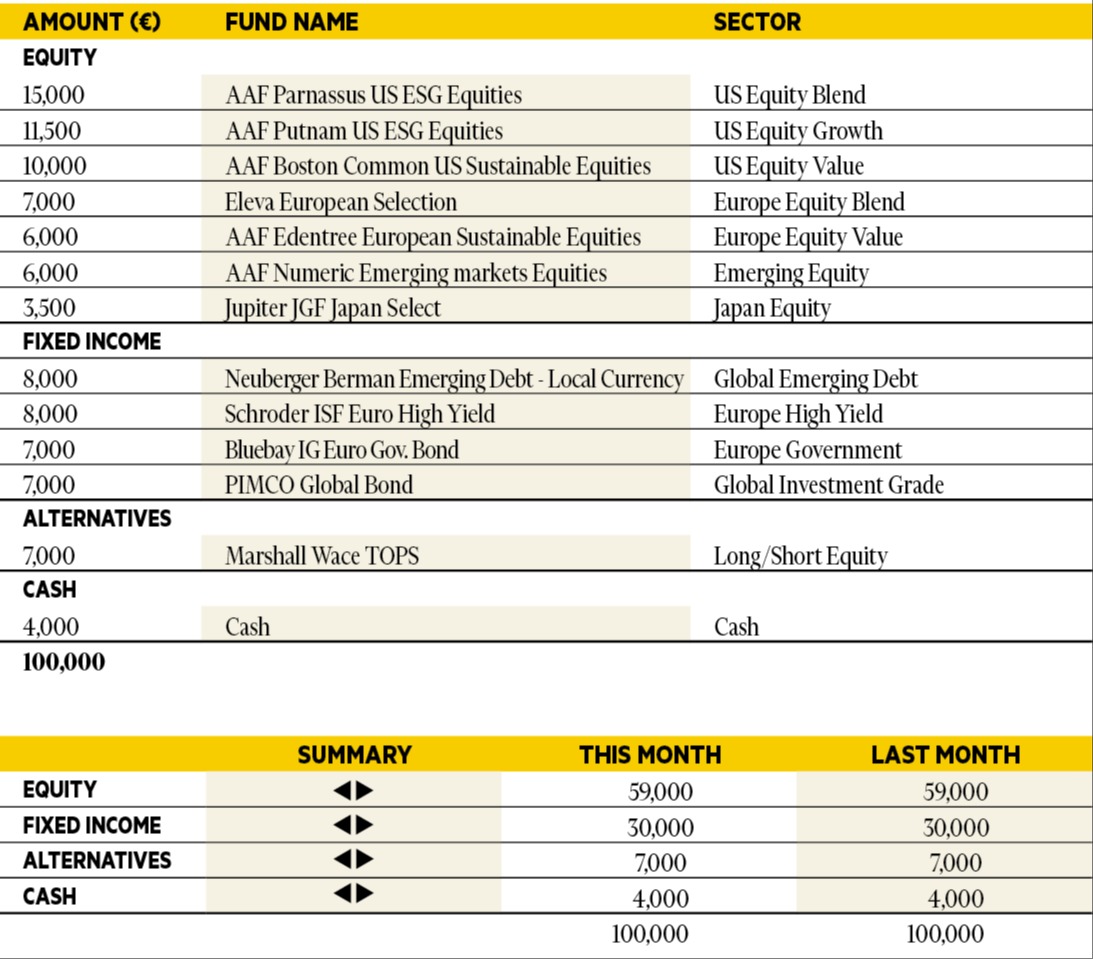

Benjamin Hamidi

Senior portfolio manager, ABN AMRO Investment Solutions.

Based in: Paris, France

“Geopolitical tensions increased recently due to the Supreme Court’s decision on tariffs, but also, and above all, because of the conflict in Iran. Although oil and gas prices have risen, they remain well below their 2022 crisis levels and far from recession territory. The key factor in the coming months will be the duration of the closure of the Strait of Hormuz. At this stage, we believe this disruption will be temporary and that the risks to the global economy remain limited. Economic activity remains broadly resilient, with most indicators still pointing toward expansion. In this context, a diversified and balanced asset allocation remains the preferred strategy and is unchanged.”

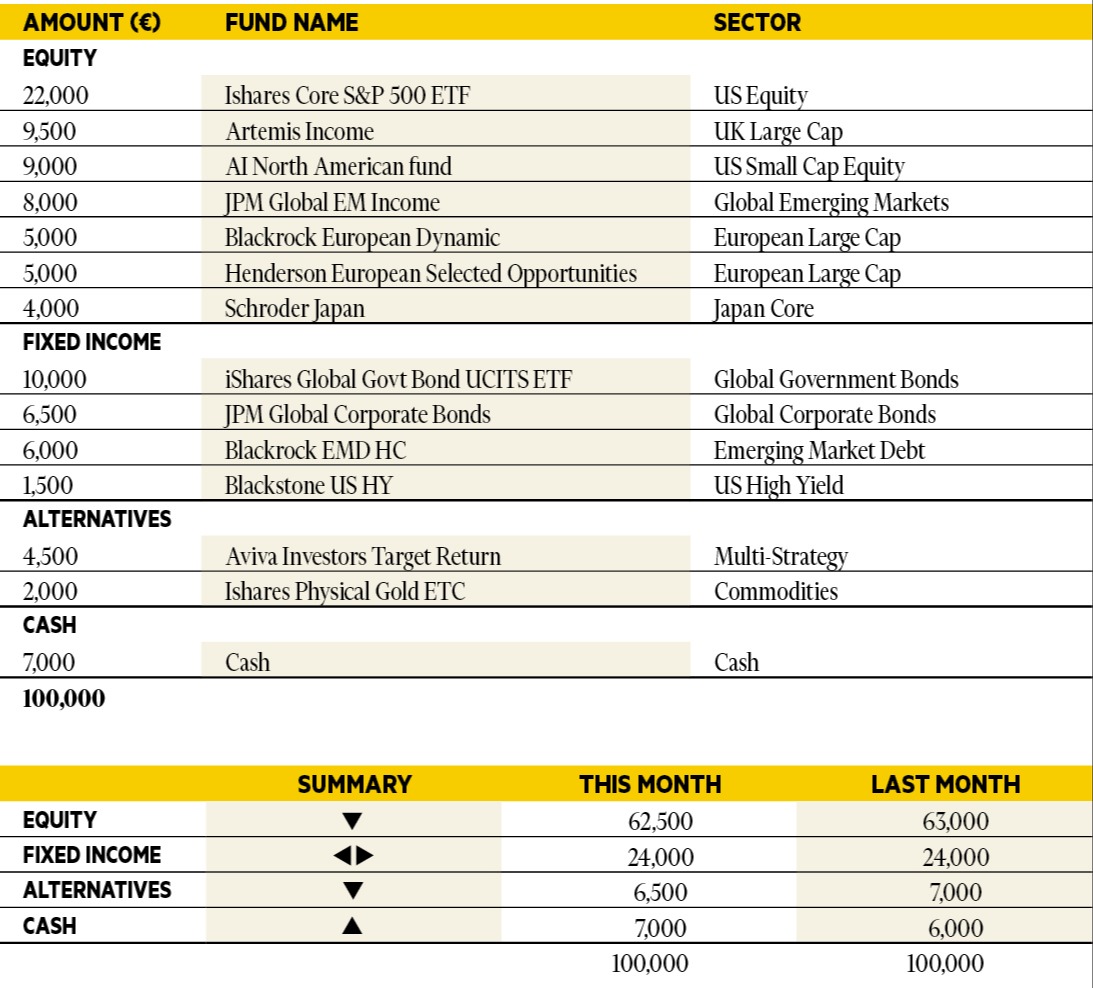

Luca Dal Mas

Senior fund analyst, Aviva Investors.

Based in: London, UK

“In the US, economic survey data moved back into expansion territory while inflation surprised modestly to the upside. Developed market equities were volatile but resilient. Early in the month, markets rotated away from crowded AI and large cap tech positions. European equities benefited from improving earnings momentum and relatively attractive valuations. Japanese equities continued to perform, supported by improving domestic data, a weaker yen and expectations of expansionary fiscal policy. The escalation in Iran triggered risk off moves and supported further sectoral rotation, with banks and technology underperforming. In portfolios we marginally rebalanced and trimmed our risk exposure across equities and precious metals.”

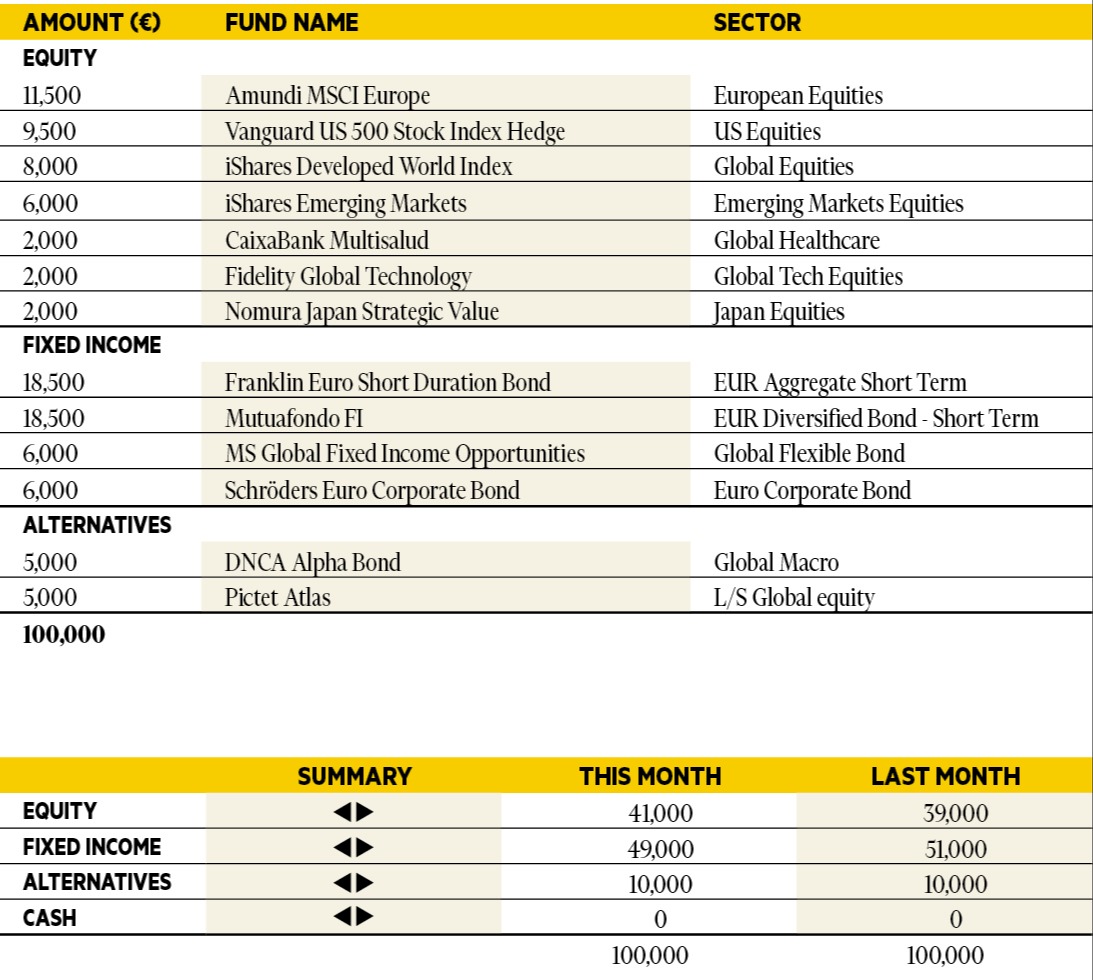

Jorge Velasco

Director of Investment Strategy, CaixaBank Private Banking.

Based in: Madrid, Spain

“The escalation of the conflict in the Middle East has triggered a renewed bout of volatility across global markets, pushing oil, gas, and gold prices higher while weighing on global equities. The situation remains highly fluid, and any firm view or definitive forecast would be overly dependent on rapidly evolving events. At this stage, our focus is on identifying the key variables that are likely to shape market pricing in the coming days, particularly given the potential of higher energy prices to act as a drag on global growth. Against this backdrop, this month we have taken a more selective approach to our geographic positioning, reducing exposure to Europe and emerging markets while increasing our allocation to US equities.”

Silvia Tenconi

Multi-manager Investments & Unit Linked, Eurizon Capital SGR.

Based in: Milan, Italy

“In February the performance of the portfolio was positive. Emerging markets, Japanese and European Equity funds were all strong contributors, while US equity funds detracted once again. Positive returns from credit, govies and also came from emerging debt. Central Banks are in a wait-and-see mode, inflation is slowly falling in the Eurozone while growth is accelerating pretty much everywhere, and in Japan the victory of Sanae Takaichi is fuelling positive expectations. Worrisome to note, geopolitical tensions are quickly rising in the Middle East, with oil rallying more than 20 per cent since the beginning of the year.”

Richard Troue

Fund Manager, Hargreaves Lansdown Fund Managers.

Based in: Bristol, UK

“The devastating escalation of conflict in the Middle East has brought energy supply and security back to the fore. Expectations for rate cuts have been pared back as all eyes turn to the inflationary impact of higher energy prices. Beyond this there are question marks over the impact a prolonged conflict could have on economic growth and the finances of already highly indebted governments. As such, government bonds have sold off heavily, while emerging markets, so strong of late, have reversed course too. History tells us it’s often best to look through geopolitical turmoil, even though it’s uncomfortable. I’m not planning any immediate changes to the portfolio, but I’ll remain vigilant to opportunities as events unfold.”

Antti Saari

Chief Investment Strategist, Nordea investments.

Based in: Copenhagen, Denmark

“Shares in some technology companies have fallen heavily in recent months due to fears that artificial intelligence will erode these companies’ revenue bases. However, other parts of the global equity market have performed very well, pulling the global market higher. The economic picture is still strong, and earnings outlook quite good. While the conflict in Middle East will keep volatility elevated in the near term, we do not believe it will significantly alter the trajectory of the equity markets overall. Therefore, we maintain an overweight in equities. We see good opportunities across the different equity regions and therefore remove the overweight in Europe.”

Didier Chan-Voc-Chun

Head of Multi-Management and Fund Research at Union Bancaire Privée (UBP)

Based in: Geneva, Switzerland

“Markets faced significant turbulence in February due to multiple factors. The US Supreme Court rejected the use of the International Economic Emergency Powers Act to justify President Trump’s April 2025 tariffs, while US-Iran tensions escalated into armed conflict after markets closed for the month. Equity investors rotated away from mega-cap US tech stocks, as strong earnings were overshadowed by concerns over AI-driven capital expenditure. Despite healthy economic activity, fears of AI-induced unemployment and rising geopolitical risks put pressure on bond yields. Over the month, we have slightly increased our exposure to emerging markets, supported by a weakening US dollar and rising commodity prices. Meanwhile, our fixed income exposure remains focused on higher-yielding segments and emerging markets to enhance carry.”